姚卫忠花了半辈子的时间经营他在杭州的家族休闲食品企业,如今已经精力不济。由于22岁的儿子对打理家族生意没有多大兴趣,姚卫忠需要新的资金和专业知识来保持公司的发展。

因此,现年48岁的姚卫忠选择了越来越多的中国企业家走过的一条路:他把自己在姚太太公司的控股权出售给了一家私募股权投资公司。

他在去年12月把这些股份卖给了总部位于上海的云月投资公司(Lunar Capital Ltd.)。“公司遇到了瓶颈,”姚卫忠上周接受电话采访时说,“我到了这个年纪已经没有足够的精力,我的孩子不愿意接手生意。我也不能强迫他喜欢。”

从金融中心上海到煤炭资源丰富的山西省,面临接班问题和经济放缓双重挑战的中国企业家越来越愿意把公司的多数股权转让给收购公司。这表明市场发生了根本性的转变,从1994年中国对私募股权投资公司开放以来,为了能分享中国经济高速增长的成果,凯雷投资集团(Carlyle Group LP)和KKR集团(KKR & Co.)等公司有时不得不放弃坚持持有所投资公司控股权的条件。

企业重组

通过买下企业控股权,收购公司可以运用他们在发达国家市场沿袭了几十年的模式:收购价值低估的公司,通过削减成本、更换管理层和调整企业战略,扭转经营状况,而不会受到根基深厚的创始人的阻挠。

“毫无争议的是,这种收购控股权的做法在中国效果更好,回报率更高,”云月投资公司合伙人苏丹瑞(Derek Sulger)说。他表示现在依然很难找到大宗交易,尤其是在科技和教育等热门领域,所以私募股权投资公司转而把注意力放在了消费和零售行业小公司的交易上。

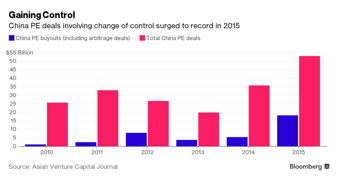

根据《亚洲创业投资期刊》(Asian Venture Capital Journal)的统计,涉及控股权变更的交易占去年中国私募股权交易总价值的34%,比2014年高出一倍以上。这家私募股权研究机构估计,不包括所谓的套利交易(通常涉及公司退市然后转到估值较高的市场上市),“控股权”交易金额从2014年的49亿美元增长到去年的68亿美元,创下历史记录。尽管如此,这类交易只占到中国私募股权交易总价值的13%。

无人接班

苏丹瑞说,他正在与至少10家中国企业进行收购谈判,这些公司的创始人或经理都打算退休或者出售控股权。其中有一家位于山西的休闲食品生产商,公司创始人的儿子去了加拿大读大学,在香港的一家投资银行工作过,现在就职于香港最大的会计师事务所之一。

“一个孩子从少年时期就离开中国,在温哥华地区的里士满长大,就读于多伦多大学,然后回国经营山西农村地区的家族企业,你怎么能指望这样一个孩子高高兴兴地接班?”苏丹瑞说,“这些企业创始人都是自尊心很强的人,他们希望看到自己的企业继续蓬勃发展,即使他们的子女不愿意接手。”

苏丹瑞说,“他们真正需要的是接班问题的解决方案,他们知道自己将面临这个问题。”

“夕阳产业”

中信资本控股有限公司(Citic Capital Holdings Ltd.)驻香港的合伙人信跃升(Eric Xin)说,他的公司正在与一家有20年历史的纺织企业谈判,这家染织企业主要向中东地区出口产品。由于该公司面临近年来销售额下降、劳动力成本上升和人民币升值的多重压力,现年46岁的老板想全部售出股权,搬到英国生活,打算让他的一个儿子在英国受教育。

“这是一家处于污染行业的工业企业,”信跃升说,“子女不希望从事这些夕阳产业,他们想当银行家和金融家。”

在许多情况下,促使中国企业家出售股权的纯粹是经济因素。2014年,中信资本收购了床垫制造商金可儿上海床具有限公司(King Koil Shanghai Sleep System Co.)的控股权。信跃升透露,中信资本在2013年末首次结识这家公司时,最大的股东并不想直接出售股份。半年后,由于该公司酒店业务的销售业绩每况愈下,库存越积越多,利润率降低,老板终于改变了主意。

云月投资的苏丹瑞说,他在寻找基本面稳健、可以通过专业化管理来解决经营难题的企业。苏丹瑞表示,以中国休闲食品企业为例,净利润率通常在4%到6%之间,只有海外竞争对手利润率的一半左右。

价格降低

中国对收购公司开放的最初几年,在能够获得控股权的少数情况下,这些公司不得不支付更高的价格。根据彭博汇编的数据显示,随着越来越多的公司进入收购名单,涉及所有权变更交易的企业价值中位数已经下降到过去12个月利润的7.2倍,远远低于2014年的11.6倍和2013年的17倍以上。

苏丹瑞说,企业老板也越来越愿意承认,他们需要私募股权公司的帮助来度过经济低迷时期,在市场营销、品牌推广和产品研发等领域掌握新的技能。

贝恩咨询公司(Bain & Co.)大中华区私募股权基金业务联席主席韩微文说,许多小企业老板从来没有应对过削减成本或进行彻底重组的困境,“这关系到降低成本、运营效率、转变业务模式和改变自身。他们从来没有做过这种事。”

反过来说,与经常发挥更积极主动的作用相比,许多收购公司也没有培养接管和重组中国企业所需的技能。韩微文说,“他们还要培养自身的能力,真正了解一家中等规模、创始人做主的私营企业如何运作。”

精神追求

姚卫忠在杭州接受采访时称,出售姚太太公司控股权(交易金额不详)的决定,让他可以专注于自己擅长的领域,比如在哪里采购产品中使用的坚果、果脯和添加剂。苏丹瑞表示,在云月投资给这家公司带来的诸多变化中,电子商务平台可能在未来创造高达20%的销售额。

对有些中国企业家来说,出售股权的主要动机是他们自己想追求更平静的生活。苏丹瑞提到,他正在谈判的两家公司老板都想退休,注重佛教等精神追求。

“由于中国经济增长现在有所放缓,你要用更睿智的方式经营企业。你必须更注重成本和电子商务等方面,”他说,“中国也面对着很多生活方式的问题。很多企业创始人想到温哥华生活和工作,很多人想投身于其他领域,比如研究佛学,还有很多人只想退休。” 撰文/Cathy Kit Ching Chan 翻译/孟洁冰 编辑/张晗

http://mobile.bbwc.cn/article/10065254/1/cat_20?articleToken=ptnu2o